As the New Financial Year starts we get reminders for Tax via our phone or through the tax men, the chartered accountant or the employer, that it is the season to plan your taxes. And your reaction would be like, again, emptying your pockets for the government that doesn’t take care of your needs!

Now think of a World that is Tax-Free. Let’s be honest. We all have fantasized about living in a world like this. But Taaadddaahhhhh lets come to reality!!!!!!!!

Apart from the fact that taxes are viewed as a financial burden, what could further add to the stress could be a lack of knowledge about tax planning. A majority of us struggle with fitting in the tax-save puzzle. Perhaps, it is high time we should start teaching taxes to students while they are still in school so that they can get prepared for this not-so-fancy term.

So the first Question for you all, What is Tax-saving and the Income Tax Act?

The Income Tax Act came into effect in 1961. Everything pertaining to the imposition, collection, recovery, and administration of income taxes falls under the purview of the Income Tax Act.

As a taxpayer, you may have multiple sources of income during your life. According to the Income Tax 1961, your earnings or profits in a given financial year attract taxes.

Whether you are a salaried individual or an entrepreneur, or whether you make a rental income, or earn an income from your investments, you have to pay taxes to the government.

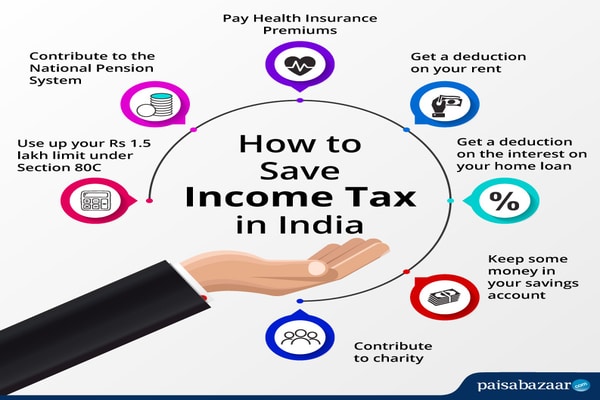

To help you in this regard, Section 80C, 80D, and 80G of the Income Tax Act list the ways you can save on taxes. If you are confused on how to plan your finances for maximum tax benefits, here are a few recommendations based on your risk appetite:

- High-risk appetite: If you are an aggressive investor and you are looking for high returns in addition to tax benefits under Section 80C, you can consider investing a total of ₹1.5 lakh per year in Equity Linked Saving Schemes (ELSS). This is a tax-saving mutual fund that has the potential to offer double-digit returns. In other words, you can avail tax benefits in the short term and earn good returns in the long term.

- Moderate risk appetite: If you have a moderate risk appetite, you can invest a portion of your money in ELSS and the rest in Public Provident Fund (PPF) and/or tax-saving fixed deposits. This strategy gives you the required tax benefits under Section 80C and also helps you balance your risk and returns.

- Low-risk appetite: If you are totally risk-averse, you can invest in saving fixed deposits or PPF. Here, you avail the same tax deduction of ₹1.5 lakh under Section 80C and the risk exposure on these avenues is minimal.

But, while these avenues offer you fixed returns, the rate of return can be quite low (just between 6-8%). This can be a problem if you take inflation into consideration. Education inflation, for instance, is around 10-12% every year. This means, if you invest in PPF for long-term goals like your child’s education, you may not be able to achieve your goals.

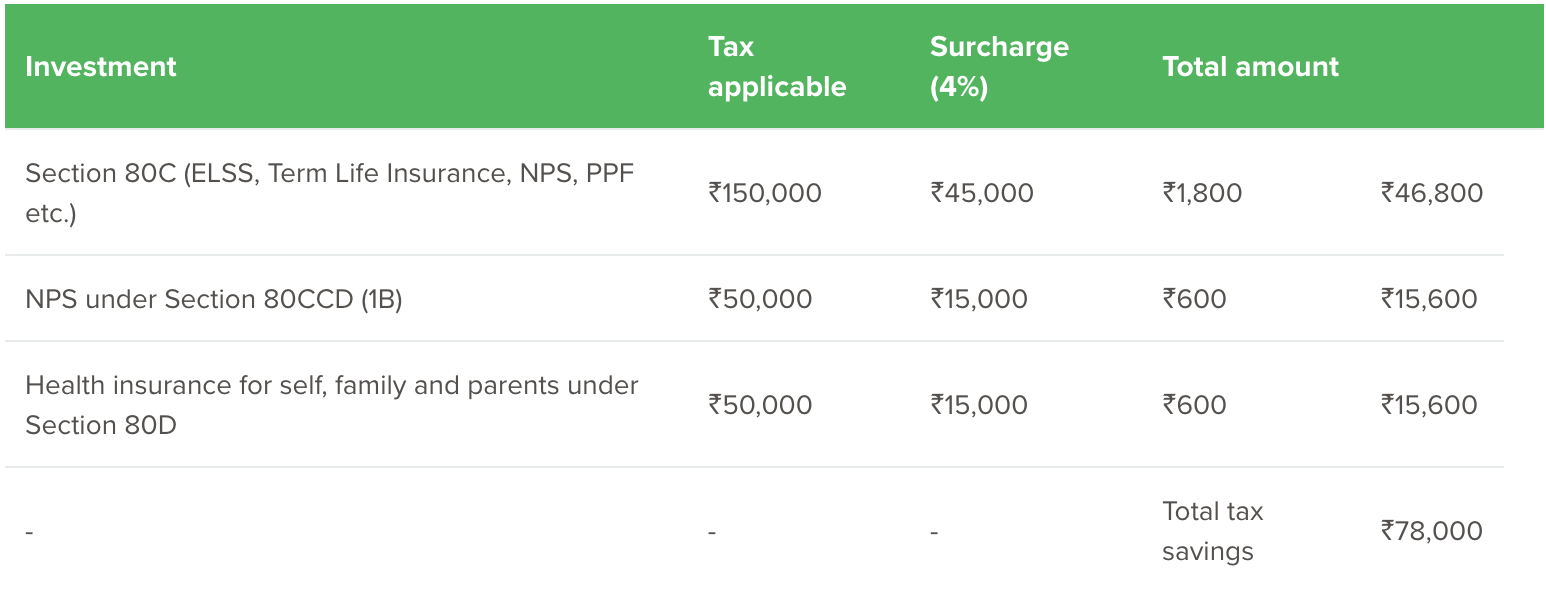

These investments can help you save a maximum of ₹46,800 on taxes every year by making these investments.

If you are still confused, no worries! By using free tools like the ET Money Income Tax calculator. you can easily save on your taxes.

Some Additional benefits beyond Section 80C

If you want deductions over and above the limit as specified under Section 80C, you can invest in the National Pension Scheme on the Atal Pension Yojana. Section 80CCD (1B) of the Income Tax Act gives deductions of up to ₹50,000 for contributions towards these schemes. As a taxpayer, you can save up to ₹15,600 under this section.

You can also claim tax benefits for premiums paid towards health insurance for self, spouse, children, and parents and term insurance plans. This benefit comes under Section 80D of the Income Tax Act. Every year, you can save up to ₹15,600 on these health insurance payments.

Overall, the combination of these options can help you save up to ₹78,000 every year. This is a considerable amount of money.

How can you save up to ₹78,000 a year?

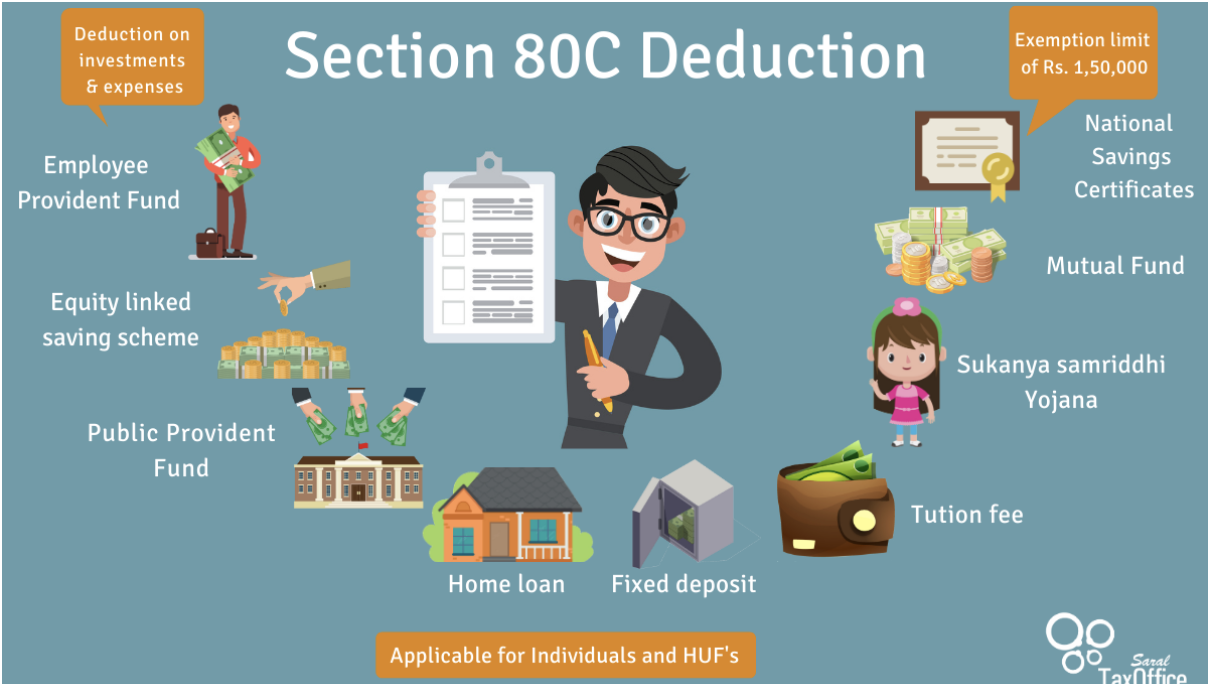

What is Section 80C?

Section 80C of the Income Tax Act 1961, reduces your tax liabilities by allowing deductions from your total taxable income in a financial year.

According to Section 80C of the Income Tax Act 1961, taxpayers can claim deduction benefits on any investments, contributions, or payments towards financial products and schemes as stipulated by the Income Tax law. Section 80C came into effect on April 1, 2006, as a replacement for the older Section 88. Currently, the maximum deduction allowed under Section 80C is ₹1,50,000 in a financial year. Earlier, until FY 2014-15, the limit was ₹1,00,000.

Then there is an Equity Linked Savings Scheme which is a type of mutual fund with a lock-in period of three years. It is the only mutual fund category in India, which qualifies for a tax deduction under Section 80(C) of the Income Tax Act. Investments are primarily made in equity markets, thus generating significantly higher returns than other tax-savings schemes in the long run. You can either choose to invest a lump sum amount or take the SIP (Systematic Investment Plan) route. However, you cannot withdraw your money before the three-year lock-in is over. Since these mutual funds invest in the stock markets, they could carry moderately high risk. However, the risk factor gets evened out in the long run, making it one of the most profitable tax-saving investments. In terms of taxes on returns, on the gains from your ELSS investments exceeding ₹1 lakh in a financial year, you have to pay an LTCG tax of 10%. If you want to earn decent returns and can stay invested in the long run, ELSS investments can be an excellent venture.

ELSS has the shortest lock-in and highest returns among all tax-saving options. And you can also escape LTCG taxes if you harvest it smartly.

You can also plan for Senior Citizen Savings Scheme; this comes in the scene when you are already retired or applying for voluntary retirement; the Senior Citizens Savings Scheme can be an option as a risk-free tax-saving investment. It is a long-term savings option backed by the Indian government. The maturity period is five years and investors can seek an extension by an additional three years. The current interest rate is 8.6%, and you can only opt for a premature withdrawal after a year of opening the account. If you close your account before two years, 1.5% of the deposit is deducted as a penalty. The interest is taxable, and TDS is applicable in case the interest exceeds ₹10,000 per annum. With an SCSS account, you can be assured of a regular income in your post-retirement years.

Then you can plan for National Pension System, which is a retirement benefit plan, administered and regulated by the Pension Regulatory Fund Authority of India. If you subscribe to the NPS, your money will be invested primarily in equity and debt instruments, and the value of the investment at maturity will depend on the performance of these asset classes. Currently, equity exposure is capped in the range of 50% to 75% and is limited to 50% for government employees. You can either decide how much money gets invested in each asset class or opt for an age-based asset allocation model. On attaining the age of 60, you can only withdraw 60% of the maturity amount; the remaining 40% is used to purchase an annuity to help you receive a pension. Premature withdrawals of up to 25% are only allowed after three years.

NPS is the cheapest equity investment product there is.

You can get linked to Term Life insurance premiums. It can allow you to avail tax deductions under Section 80C. Premiums paid to ensure self, spouse, dependent children and any member of Hindu Undivided Family are eligible. If the policy has been issued on or before March 31, 2012, the annual premium up to 20% of the assured sum becomes tax-deductible. For insurance policies issued on or after April 1, 2012, 10% of the sum assured is tax-deductible. A life insurance policy will provide your family financial support in case of your untimely death and should be taken by everyone. The tax benefit is an added perk. Choose a life insurance plan appropriate for you and your family. It is important not to view insurance cover only as a way to save taxes.

HERO OF MIDDLE CLASS is Public Provident Fund, which is a long-term investment option through which you can also avail tax benefits. The current rate of interest on a PPF account is 7.9% p.a., compounded annually, and the lock-in period is 15 years. This means you have to stay invested for 15 years, although partial withdrawals are allowed from the seventh year. You can open an account with as little as ₹100. The minimum and maximum investments allowed in a financial year are ₹500 and ₹1.5 lakh, respectively. In case your annual investment exceeds ₹1.5 lakh, interest cannot be earned on the excess amount. You will have to make at least one deposit a year for 15 years. PPF is regarded as a safe tax-saving investment avenue. You do not have to pay any taxes on the deposit or interest at the time of withdrawal.

Government allows you to move entire PPF corpus to NPS and enjoy better returns and flexibility.

You can also opt for National Savings Certificates. It is a fixed-income investment offered by the Government of India. You can invest in this scheme by visiting a post office near you. The lock-in is five years, and the current interest rate is 7.9% per annum. The minimum amount required to purchase an NSC certificate is ₹100. Certificates are available in denominations of ₹10,000, ₹5,000, ₹1,000, ₹500, and ₹100. Premature withdrawals are only allowed if the certificate holder has passed away, or if the certificates have been forfeited. The scheme is safe as it is backed by the Government of India which ensures the safety of your capital. Also, only the interest earned in the final year is taxed.

Try on Tax-saving FDs where you can invest in tax-saving fixed deposits and claim maximum tax deductions of up to ₹1.5 lakh. The interest rate you get is what the prevailing 5 year FD rate is and the lock-in period is five years, which means you can’t take out the money before five years. You can only make a one-time lump sum deposit, while premature withdrawals are not allowed. The minimum investment amount varies depending on your bank, but the maximum amount is capped at the 80C limit, i.e. ₹150,000. You can either reinvest the interest or opt for monthly or quarterly payouts. TDS is applicable on the interest earned on your FD, but you can avoid it by submitting Form 15G or Form 15H (in case you are a senior citizen) to the bank.

Tax saving FDs provide just enough returns to beat inflation. So, technically your wealth gain are negligible.

- Home loan repayment: If you have taken a home loan, the part of EMI that goes towards repaying the principal amount is eligible for tax deductions under Section 80C. The amount you pay as interest does not qualify for tax deductions under this section.

- Tuition fees: You can claim tax deductions up to ₹1.5 lakh on tuition fees paid for your child’s education. This benefit is only available to individual parents or guardians and a maximum of two children per individual. The deduction does not depend on the class of the child. However, it must be a full-time education course in an Indian school, college or university. Parents of adopted children, unmarried individuals and divorced parents can also claim these benefits.

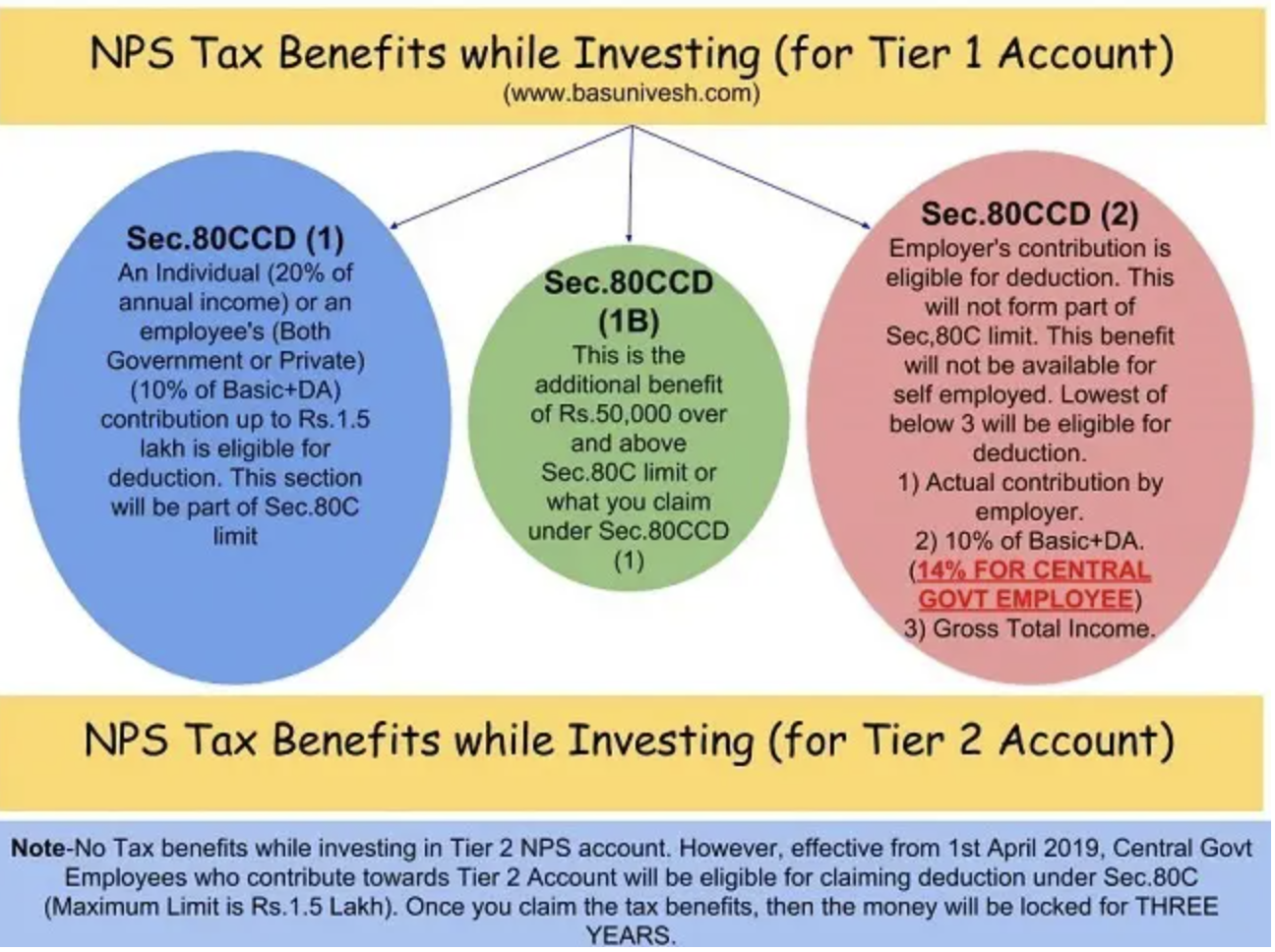

What is Section 80CCD?

Section 80CCD discusses the tax deductions available to taxpayers regarding investments in the National Pension System (NPS). There are two subsections here:

- Section 80CCD (1): Investments in NPS are eligible for tax deductions under this section. Any Indian citizen between the age of 18 and 60 years can invest in NPS and avail this tax benefit. Even NRIs can claim this benefit. The maximum deduction you can avail of under this section is 10% of your salary (this includes basic salary + DA). For self-employed individuals, the limit is 20% of their gross total income.

Also, the maximum benefit you can avail of every year under this section is ₹1.5 lakh.

- Section 80CCD (1b): This subsection provides an additional deduction of ₹50,000 on investments in NPS. This is over and above the ₹1.5 lakh available under Section 80CCD(1). So, in short, you can avail a total tax deduction of ₹2 lakh when you invest in NPS every year.

What is Section 80D?

Under Section 80D of the Income Tax Act, you can claim deductions up to ₹1 lakh for contributions towards medical insurance premiums bought for insuring self, spouse, children and parents. . The deductions under 80D are over and above the exemptions, you can claim under Section 80C. This benefit can be claimed by individuals and Hindu Undivided Families (HUFs).

If you file your taxes as an individual, you can claim deductions for insuring yourself and your family. In addition:

- You can claim a maximum deduction of ₹25,000 in a financial year on the health insurance premium for self and family, i.e., spouse, parents and children.

- If you are a senior citizen, you can claim a maximum deduction of ₹50,000 per financial year.

- Here are the provisions for premiums bought for medical insurance for parents.

- If your parents are less than 60 years of age, you can claim a maximum deduction of ₹25,000 per year on their health insurance premiums bought on their behalf.

- If they are senior citizens, the maximum deduction allowed is ₹50,000 in a financial year.

Overall, if you purchase a life insurance policy for your family as well as your parents (and your parents are below the age of 60), you can claim a maximum tax deduction of ₹50,000. But if you and your parents are above the age of 60, you can avail of a maximum deduction of ₹1 lakh under Section 80D.

What is Section 80E?

Under Section 80E of the Income Tax Act, the amount you spend in repaying the interest on your education loan can qualify as a deduction from your total income.

The loan should have been taken for the education of self, spouse, children, or a student for whom you are the legal guardian, and should have been taken from a bank or an approved financial institution.

The total amount paid in repaying the loan interest in a financial year is regarded as the deduction amount and there is no cap on the maximum amount you can claim as a deduction. You will have to acquire a certificate from the bank that differentiates the principal from the interest component of the education loan you have repaid.

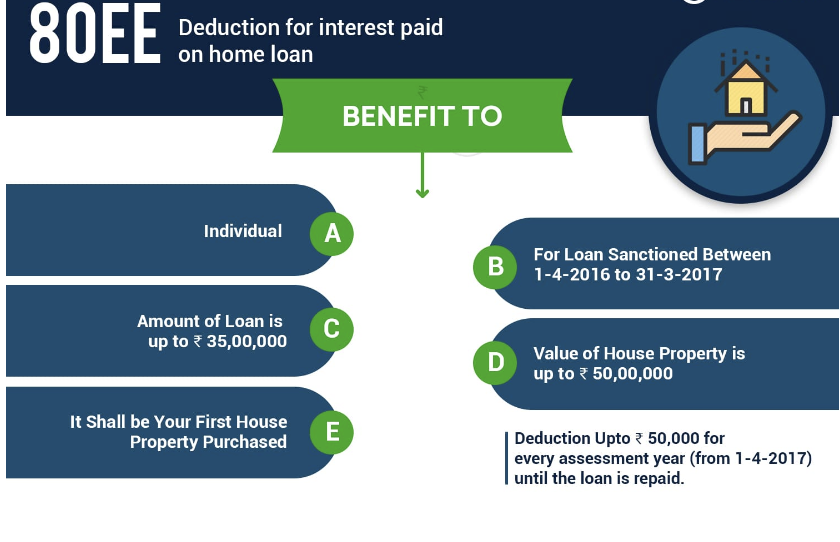

What is Section 80EE?

Section 80EE of the Income Tax Act, 1961 allows a tax deduction benefit on the interest paid on home loans taken by a first-time homebuyer. If you fall into this category, you can claim a tax deduction of up to ₹50,000 under section 80EE. This deduction limit is over and above the limit provided under section 80C and Section 24 of the IT Act, 1961.

Section 80EE of the Income Tax Act, 1961 allows a tax deduction benefit on the interest paid on home loans taken by a first-time homebuyer. If you fall into this category, you can claim a tax deduction of up to ₹50,000 under section 80EE. This deduction limit is over and above the limit provided under section 80C and Section 24 of the IT Act, 1961.

As a taxpayer, you need to satisfy the following conditions to be eligible to claim this deduction.

- You should not own any other residential property on the date of the sanction of the loan.

- The value of the house should be less than ₹50 lakh. The loan must not be availed for a commercial property.

- The loan amount needs to be less than ₹35 lakh.

- The deduction is only available on the interest portion of the loan.

- You do not necessarily have to reside in that property to be eligible.

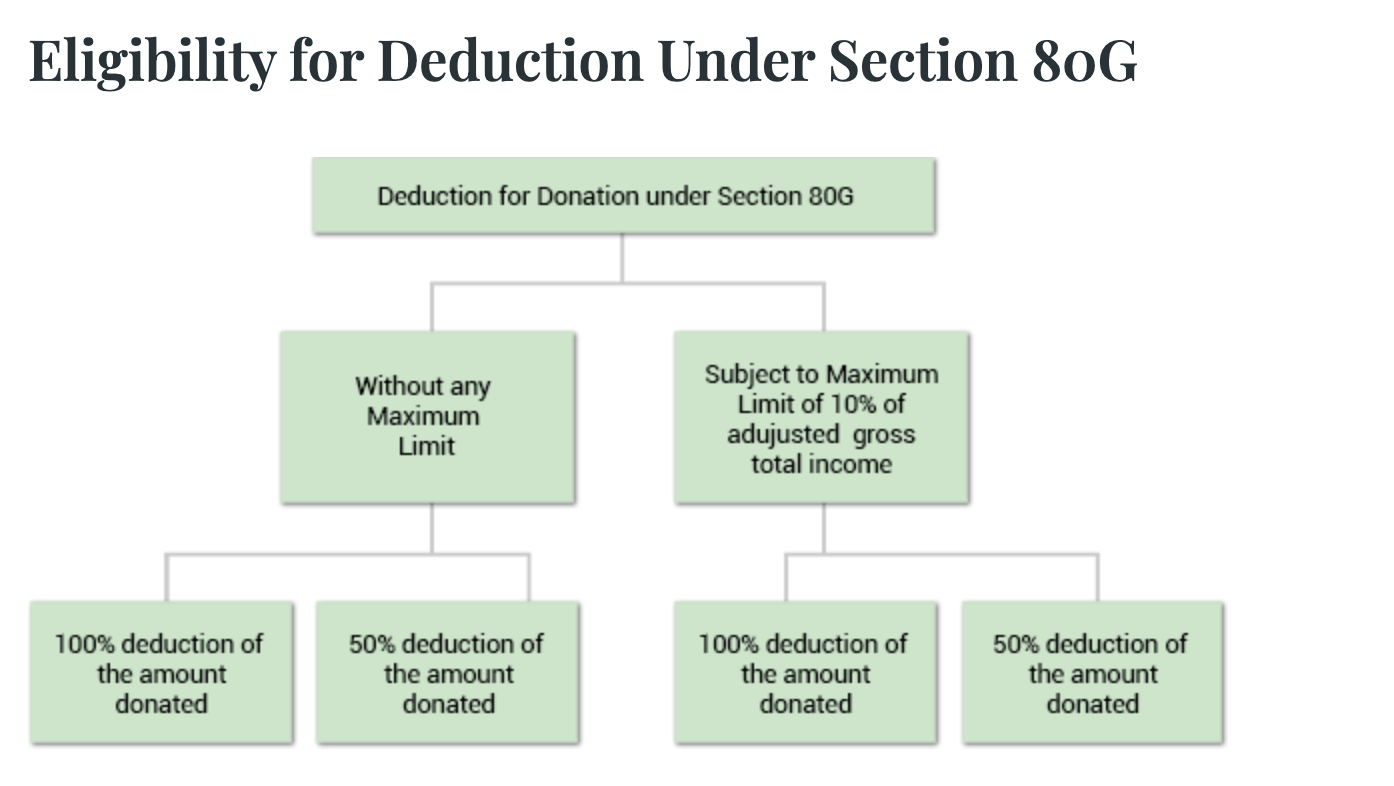

What is Section 80G?

Charity begins at home, but did you know that if you widen the scope of your charitable acts, it can help you save taxes? Section 80G of the Income Tax Act allows you to claim tax deductions on donations made to charitable organizations.

Only donations made towards charitable institutions registered under Section 12A can qualify for deductions. The donations must have been made through taxable income sources. Only those donations where contributions have been made via cash or cheque or demand draft will be eligible. All taxpayers, including non-resident Indians, are eligible.

Cash donations exceeding ₹2,000 are not allowed as a deduction. For donations above ₹2,000 to qualify as a tax deduction, the contribution has to be made using other modes of payment. The various contributions are eligible for a deduction of up to either 100% or 50%, with or without restriction, under Section 80G.

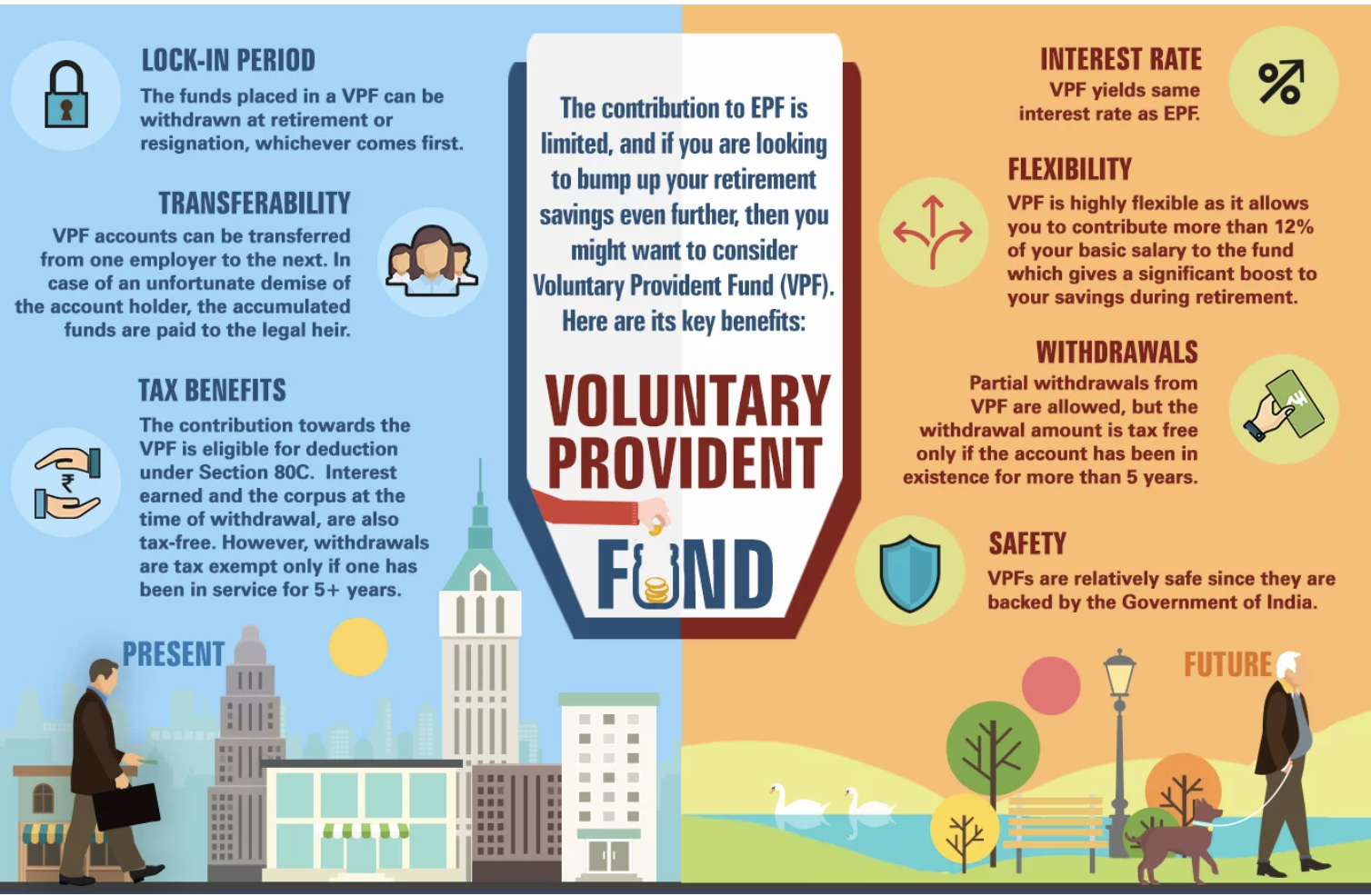

You can also try for VPF Withdrawal

VPF allows partial withdrawals and complete withdrawals. This is a good option to fall back on in case of any unforeseen financial emergencies like paying hospital bills for yourself and/or your family. You can also break your VPF account open for reasons such as:

- Construction or purchase of a new house or a residential plot

- Repayment of an existing home loan

- Higher education or marriage of a child

VPF is quite popular among investors because the accumulated amount can be withdrawn at any point in time. But ensure that your account is active for five years at least if you want to avoid paying tax on the maturity amount.

Always be on the EPFO portal with your UAN Number

The Universal Account Number (UAN) is a 12-digit number, allotted by the Employee Provident Fund Organization to every employee having an EPF account. The UAN remains constant throughout the life of an employee and is portable.

The primary benefit under the UAN is that you do not need to withdraw your EPF when you change jobs. You can transfer your EPF from an old employer to a new one quickly and without hassle. Hence, regardless of the number of times you change your job, you can continue building your EPF corpus without a break.

Then the question arises, What are the Advantages of UAN to Employees?

- You can transfer your EPF balance from an old account to a new one through the UAN.

- Each new PF account with a new job will come under the aegis of a single unified account.

- Whenever you need your PF statement, you can download one instantly – either by logging in using your member ID or UAN or by sending an SMS.

- New employers do not need to validate your profile if the UAN has been Aadhaar and KYC-verified.

- It can be easier to withdraw (fully or partially) EPF online with UAN.

- It is easier for you to ensure that your employer is regularly depositing their contribution in the PF account.

Conclusion of this Whole Discussion

As an employee, you can be assured of a retirement corpus from the EPF scheme. And throughout your career, if you’ve moved jobs, you can be assured of availing the benefits of the provident fund under the same umbrella account, courtesy of the UAN. The VPF (if you choose to invest) provides additional protection and cover.

But on the flip side, EPF has certain limitations. When it comes to investment returns, other retirement saving options like National Pension System (NPS) or Equity Linked Saving Scheme (ELSS) have the potential to earn higher returns. In addition, even VPF comes with restrictions. You can make a full withdrawal from your VPF account only at the time of retirement. This can pose a challenge if you want to meet other financial goals in the short term. A good alternative is to invest in NPS or ELSS if you want inflation-beating returns for your retirement.

Your article helped me a lot, is there any more related content? Thanks! https://www.binance.com/register?ref=JW3W4Y3A

Your article helped me a lot, is there any more related content? Thanks! https://www.binance.com/join?ref=IHJUI7TF

зубной детский стоматолог лечение зубов детям под наркозом

ремонт ванна ключ цена https://remont-vannoy-spb.ru

Need a multimedia system? equipment for meeting rooms We integrate multimedia systems for home and business. We install and configure audio and video systems, manage content, and integrate equipment into a single system. Modern solutions for comfortable and efficient use of technology.

Подробности на странице: https://elicebeauty.com/makiyazh/litso/osnovy-pod-makiyazh/osnova-pod-makiyazh-vipera-photo-model.html

Хочешь казино бонус? топ новых бонусов без депозита всегда актуальные бонусы в онлайн казино. Получайте бонусы без вложений, фриспины и подарки за регистрацию. Актуальные предложения, честные условия отыгрыша и список проверенных казино с бонусами без депозита.

Лучшие казино рейтинг онлайн казино: актуальный список онлайн казино с высоким рейтингом, быстрым выводом средств и выгодными бонусами. Обзор лицензий, игр и платежных методов поможет выбрать надежное казино для комфортной игры.

Халява казино фриспины без депозита за регистрацию: фриспины за регистрацию, бонусы без пополнения и акции для новых игроков. Сравнивайте условия отыгрыша, выбирайте проверенные онлайн казино и начинайте играть бесплатно с возможностью вывода выигрыша.

Лучшие фриспины 2026 бездепозитный бонус за регистрацию: бесплатные вращения в онлайн казино без вложений. Подборка проверенных сайтов, бонусы за регистрацию, честные условия отыгрыша и возможность вывода выигрыша без риска для игроков.

Официальный сайт покерок скачать: регистрация, вход, бонусы и игра в онлайн покер. Обзор возможностей, турниров, кеш-столов и мобильного приложения. Узнайте, как начать играть и выводить деньги на проверенной платформе.

Use this free vin lookup to decode any vehicle identification number and get full specifications instantly.

This resource this service helps verify vehicle condition and reveals hidden damage or title problems.

Reliable platform https://privatejetcharterfly.com provides access to verified charter fleet ranging from light to heavy jets.

Check http://www.rentprivatejetfly.com to compare private jet rental costs and find the best hourly rates instantly.

Нужен дизайн участка? ландшафтный дизайн дачного участка проектирование и благоустройство участка с учетом рельефа, растений и стиля. Создаем красивые и функциональные решения для частных домов и дач, подбираем материалы и обеспечиваем качественную реализацию проекта.

Брендирование сувениров https://4youcreation.kz в Алматы по современным технологиям. Специалисты предлагают лазерную гравировку, УФ-печать и термоперенос на ткани, стекло, металл и пластик. Организуют доставку по всему Казахстану.

Компания FarbWood https://farbwood.by предлагает пиломатериалы из сибирской лиственницы для частного и коммерческого строительства в Минске и по всей территории Минска. Мы работаем только с лиственницей сибирской, сосна и ель используются как дополнение к основному ассортименту древесины.

Нужна накрутка соц сетей? накрутка лайков тик ток увеличение подписчиков, лайков и просмотров для продвижения аккаунтов. Быстрый старт, безопасные методы и живая активность помогут развить профиль и повысить вовлеченность в популярных социальных платформах.

The best porn generator best nsfw ai generator your fantasies remain strictly between you and the neural network. Instant, high-quality generation, extensive scenario and character customization.

Самое важное сегодня: https://dimonvideo.ru/usernews/catalog_74/422059

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Certified platform discord aged accounts online tracks account health metrics proactively and notifies buyers of any status changes during the guarantee period. Every account goes through rigorous testing for login stability, platform trust signals, and checkpoint clearance before being listed in the catalog. Competitive pricing, fast delivery, and professional support make this a preferred choice for serious media buyers.

Modern platform tik tok business manager caters to solo buyers and agencies who need reliable accounts at scale with volume pricing and priority restocking. Orders are processed through a secure checkout system with multiple payment options and encrypted credential delivery via personal dashboard. Every order comes with clear documentation, replacement guarantees, and access to a growing knowledge base of operational resources.

Full-service dealer buy aged gmail accounts 2026 goes beyond selling by providing operational guides, restriction breakdowns, and platform update summaries. The knowledge base includes working guides for account warming, ad launch protocols, and reinstatement check procedures for reference. A single trusted supplier for all account needs simplifies operations and reduces the risk of working with unverified sources.

Full-service dealer buy instagram account verified online goes beyond selling by providing operational guides, restriction breakdowns, and platform update summaries. The selection includes profiles sorted by registration method, warming protocol, age, and included assets so buyers can match accounts to their specific needs. From first purchase to ongoing scaling, the platform supports every stage of a media buyer’s operational journey.

Reputable service mcc account google ads publishes detailed product cards showing account age, verification status, included assets, and exact pricing tiers. The selection includes profiles sorted by registration method, warming protocol, age, and included assets so buyers can match accounts to their specific needs. A single trusted supplier for all account needs simplifies operations and reduces the risk of working with unverified sources.

Verified marketplace buy hotmail account provides access to a wide catalog of digital profiles for advertising and media buying. Detailed usage guides help buyers understand the differences between softreg, selfreg, farmed, and reinstated account types before purchasing. A single trusted supplier for all account needs simplifies operations and reduces the risk of working with unverified sources.

Specialized store reddit marketing agencies that prevent shadowbans focuses exclusively on accounts proven to perform in paid advertising with real spend history and trust indicators. A loyalty program with cashback on every order makes repeated purchases more cost-effective for teams with regular sourcing requirements. From first purchase to ongoing scaling, the platform supports every stage of a media buyer’s operational journey.

Reliable source protonmail multiple accounts connects advertisers with thoroughly vetted profiles backed by replacement guarantees and dedicated support. Orders are processed through a secure checkout system with multiple payment options and encrypted credential delivery via personal dashboard. Teams that prioritize account quality over raw volume consistently achieve better ROI and fewer campaign interruptions.

Cost-effective marketplace buy yahoo pva accounts offers competitive rates without compromising on account quality, verification completeness, or delivery speed. The platform combines speed and reliability — most products are delivered automatically within minutes after payment confirmation. Invest in verified account infrastructure and redirect the time saved from troubleshooting into actual campaign optimization work.

Established supplier kick vs twitch vs youtube for new streamers 2026 maintains the largest selection of quality accounts with transparent specs and competitive pricing for bulk buyers. Step-by-step documentation accompanies every order, covering login procedure, security setup, and recommended first actions after access. Experienced buyers return for the consistency — same quality standards, same fast delivery, same professional support every time.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

интерьер дизайнер дизайн студия спб интерьера

спб дизайн дизайн интерьера для квартиры

дизайн проект интерьера коттеджа дизайн проект домов под ключ

The best porn generator porngen your fantasies remain strictly between you and the neural network. Instant, high-quality generation, extensive scenario and character customization. Available 24/7. For adults.

Больше на нашем сайте: https://www.magcloud.com/user/dezavtor

Detailed comparisons bestguitarreview make it easy to choose between acoustic and electric guitar models.

Music producers best headphone brands rely on expert reviews to choose the best studio headphones for mixing.

Online resource best microphone for vocals helps creators compare microphone prices features and professional sound quality.

Последние обновления: высокополигональная модель для агр

Советы автомехаников https://proavtomaster.com полезные рекомендации по ремонту и обслуживанию автомобиля. Узнайте, как продлить срок службы двигателя, подвески и электрооборудования, избежать частых поломок и сэкономить на ремонте благодаря практическим советам специалистов.

Профессиональный автосервис https://km-motors.org кузовной ремонт, покраска авто, ремонт двигателя и подвески. Компьютерная диагностика, автоэлектрика, ТО, замена масла, фильтров и шиномонтаж. Работаем быстро, качественно и по стандартам производителей.

Компания «Заборыч» https://заборыч.рф более 10 лет осуществляет строительство заборов из профнастила и сетки рабицы. Мы производим заборы для частных лиц и производственных объектов. За это время мы построили десятки объектов, от простых ограждений до сложных ландшафтных комплексов. Наши клиенты остаются довольны качеством работ и сроками реализации проектов.

смотреть порно шлюхи зрелые шлюхи

Профессиональная помощь детям https://neuropsy-centr.ru с нарушениями речи и развития. Высококвалифицированные врачи, работаем с самыми тяжелыми случаями, 99% положительных отзывов, новейшее оборудование и инвентарь. Государственная лицензия: Л035-01298-77/01604531 от 09.12.24

Платная частная клиника https://mypsyhealth.ru/services/psikhiatricheskaya-klinika психиатрии, неврологии и наркологии — анонимное лечение и консультации специалистов. Диагностика, помощь при зависимостях, неврологических и психических расстройствах. Конфиденциальность, опытные врачи и комфортные условия.

дом ключ модульный модульный дом что это такое простыми словами

Узнать больше здесь: https://russkoitalslovar.ru/letter/%d0%a6

Скоро лето и жара купить кондиционеры с установкой в москве широкий выбор сплит-систем для квартиры, дома и офиса. Поможем подобрать модель по площади, бюджету и характеристикам. Установка под ключ, гарантия, доставка и выгодные цены на популярные бренды.

Top web design https://webdesignfirmshub.com companies worldwide: a selection of the best studios for website and interface creation. Learn about case studies, design approaches, UX/UI solutions, and innovations to help you choose a reliable contractor for your digital projects.

Top branding agencies https://topbrandagencies.com worldwide: the best studios for brand development, corporate identity, and positioning. Portfolio reviews, strategies, and case studies will help you choose a reliable agency for business development and brand enhancement.

Top UX/UI design https://uiuxagencies.com agencies: the best companies creating user-friendly interfaces and digital products. Explore case studies, methodologies, and approaches to UX/UI to choose a reliable contractor for your website or app.

Дубликаты номеров https://avtostrahovka36.ru в Воронеже — изготовление и восстановление регистрационных знаков по ГОСТ. Срочно за 1 день, качественные материалы, соответствие требованиям и выгодные цены. Оформление быстро и без очередей.

A non-profit organization https://linkimpact.org dedicated to supporting multicultural families, environmental protection, volunteerism, and language and cultural exchange.

Практик о заборах sinta-kedr.ru честный разбор материалов, установки и стоимости. Узнайте плюсы и минусы разных видов заборов, частые ошибки и реальные сроки службы. Полезные рекомендации перед покупкой и монтажом ограждений.

An astrology portal burcler com az with daily horoscopes, natal charts, and forecasts. Online consultations, zodiac sign compatibility, and personalized recommendations will help you better understand yourself and make important decisions.

Дубликаты номеров https://avtostrahovka36.ru в Воронеже — изготовление и восстановление регистрационных знаков по ГОСТ. Срочно за 1 день, качественные материалы, соответствие требованиям и выгодные цены. Оформление быстро и без очередей.

Практик о заборах https://sinta-kedr.ru/ честный разбор материалов, установки и стоимости. Узнайте плюсы и минусы разных видов заборов, частые ошибки и реальные сроки службы. Полезные рекомендации перед покупкой и монтажом ограждений.

Все новостройки https://tut-novostroyki.ru от застройщиков в Новосибирске — актуальный каталог квартир в новых ЖК. Цены, планировки, сроки сдачи и акции. Подберите квартиру напрямую от застройщика без комиссии с удобным поиском и проверенной информацией.

Дизайнерское бюро https://vseremontytut.ru проектирование интерьера и ремонт под ключ. Разработка дизайн-проекта, 3D-визуализация, подбор материалов и полная реализация. Создаем стильные и функциональные пространства с гарантией качества и соблюдением сроков.

Шпаклевка стен https://shpaklevka-sten.ru и потолков в Москве — выравнивание поверхностей под покраску и обои. Качественные материалы, опытные мастера и соблюдение технологий. Выполняем работы быстро, аккуратно и с гарантией результата по доступной цене.

Бытовая химия в Казани https://bytovayalavka.ru широкий ассортимент средств для уборки, стирки и ухода за домом. Оригинальная продукция, выгодные цены и быстрая доставка. Подберите качественные моющие средства для чистоты и комфорта вашего дома.

Механизированная шпаклевка https://shpaklevka-msk.ru современный способ выравнивания стен и потолков. Ровное нанесение, высокая скорость работ и экономия материалов. Подготовка под финишную отделку с гарантией качества и соблюдением технологий.

Calculate your horoscope https://www.ulduz-fali.com.az online. Horoscopes, love compatibility, daily horoscopes and astrological interpretations by date of birth on one site.

Dream Interpretations 2026 https://www.yuxu-yozmalari.com.az learn the meaning of your dreams with AI artificial intelligence. Dream interpretation from A to Z, folk belief interpretation, psychological approach. Free online dream interpretation.

Жіночий сайт https://zhinka.in.ua поради про красу, здоров’я, стосунки та стиль життя. Читайте корисні статті, лайфхаки, рецепти догляду та натхнення для сучасних жінок. Все про жіночу гармонію, саморозвиток і комфорт у повсякденному житті.

Сайт міста Вінниця https://faine-misto.vinnica.ua новини, події, довідник компаній і корисна інформація для жителів та гостей. Актуальні новини, афіша, транспорт, послуги і все про життя міста в одному зручному онлайн-порталі.

An online numerology https://numerologiya.com.az profile analyzes your destiny, talents, and finances. Accurate calculations, number interpretation, and personalized recommendations will help you better understand yourself and choose the right direction in life.

Сайт міста Одеса https://faine-misto.od.ua новини, події, афіша, довідник компаній та корисна інформація. Дізнавайтесь актуальні новини, знаходьте послуги, заклади і маршрути. Все про життя Одеси для мешканців і гостей міста в одному місці.

Сайт міста Житомир https://faine-misto.zt.ua новини, події, афіша та довідник компаній. Актуальна інформація про життя міста, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Житомира в одному зручному онлайн-порталі.

Автомобільний портал https://avtogid.in.ua новини авто, огляди, тести та поради водіям. Дізнавайтесь про нові моделі, технології, ремонт і обслуговування. Все про автомобілі в одному місці для власників і автолюбителів.

Сайт міста Львів https://faine-misto.lviv.ua новини, події, афіша та довідник компаній. Актуальна інформація про життя міста, транспорт, послуги і заклади. Усе необхідне для мешканців і туристів Львова в одному зручному онлайн-порталі.

Блог Києва https://infosite.kyiv.ua події, новини, цікаві місця та корисні поради для мешканців і гостей столиці. Дізнавайтесь про актуальні заходи, життя міста, розваги та сервіси. Все найцікавіше про Київ в одному зручному онлайн-блозі.

Сайт Полтави https://u-misti.poltava.ua новини, події, афіша та довідник компаній міста. Актуальна інформація про життя, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Полтави в одному зручному онлайн-порталі.

У місті Одеса https://u-misti.odesa.ua актуальні новини, події, афіша та корисна інформація для мешканців і гостей. Дізнавайтесь про життя міста, транспорт, заклади і послуги. Все найважливіше про Одесу в одному зручному онлайн-порталі.

Житомир онлайн https://u-misti.zhitomir.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Житомирі в одному місці.

Хмельницький онлайн https://u-misti.khmelnytskyi.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Хмельницькому в одному місці.

Київ онлайн https://u-misti.kyiv.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Києві в одному місці.

У місті Львів https://u-misti.lviv.ua актуальні новини, події, афіша та корисна інформація для мешканців і гостей. Дізнавайтесь про життя міста, транспорт, заклади і послуги. Все найважливіше про Львів в одному зручному онлайн-порталі.

У місті Вінниця https://u-misti.vinnica.ua новини, афіша заходів, довідник закладів і корисні сервіси. Дізнавайтесь про події, відкривайте нові місця і плануйте свій час у Вінниці легко та зручно.

Міський сайт Дніпра https://u-misti.dp.ua новини, події, оголошення і довідник організацій. Зручний пошук послуг, закладів і маршрутів. Будьте в курсі життя міста та знаходьте потрібну інформацію швидко.

Где можно познакомиться https://datenow.ru в России в 2026 году? Приложения для знакомств стали главным инструментом для миллионов. Но важно выбрать те, где реально можно найти человека для отношений. Не просто лайки, а искренний интерес. Разбираем, какие сервисы работают в этом году. Честно. Без рекламы. Только для тех, кто ищет всерьёз.

Сайт Чернівців https://u-misti.chernivtsi.ua новини, події, афіша та довідник компаній міста. Актуальна інформація про життя, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Чернівців в одному зручному онлайн-порталі.

Міський сайт Черкас https://u-misti.cherkasy.ua новини, події, оголошення і довідник організацій. Зручний пошук послуг, закладів і маршрутів. Будьте в курсі життя міста та знаходьте потрібну інформацію швидко.

Только лучшие материалы: https://petrovskaya-rivera-novostroy.ru

Полная статья здесь: https://dom-u-nevskogo-novostroy.ru

Наша лучшая подборка: https://domstav.ru

дизайн проект квартиры для ремонта дизайнеры интерьера санкт петербурга

дизайн студия спб интерьера студии дизайна интерьеров

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://accounts.binance.com/register-person?ref=IXBIAFVY

ТОП лучших МФО https://mfo-finance.github.io проверенные компании с высоким уровнем одобрения займов. Актуальные предложения, прозрачные условия, быстрые выплаты и онлайн оформление. Сравнивайте и выбирайте надежные МФО для получения денег.

Are you into rafting? https://tara-montenegro-rafting.me/ exciting rafting trips down mountain rivers with experienced instructors. A tour of the Tara Canyon offers scenic routes, safety, and unforgettable experiences. Book a rafting tour and discover an active holiday.

dental problems? dental tourism high-quality dental treatment abroad at affordable prices. Implants, veneers, prosthetics, and treatments with a guarantee. We select a clinic, organize your trip, and provide patient support throughout the entire process.

Zahnprobleme? https://www.zahntourismus-in-montenegro.com zahnbehandlung im Ausland mit bis zu 70 % Ersparnis. Implantate, Zahnersatz, asthetische Zahnheilkunde und Diagnostik in modernen Kliniken. Wir unterstutzen Sie bei der Wahl des Landes und der Klinik und organisieren Ihre Reise von A bis Z.

Студия дизайна https://dill-design.ru интерьера в Санкт-Петербурге. Реализовываем проекты в г. Санкт-Петербург и г. Москва. Более 100 довольных заказчиков доверили нам создание своего интерьера. От разработки дизайн проекта до его качественной реализации. Авторский надзор на всех этапах реализации. Комплектация в подарок. Закажите расчет дизайн-проекта

Обзор путешествий https://tfast.ru и экскурсий. Ваш персональный гид в мире путешествий. Мы собираем самые живые обзоры, проверенные маршруты и уникальные экскурсии — от известных достопримечательностей до скрытых мест, о которых знают только местные. Планируйте свои приключения с нами, вдохновляйтесь и открывайте мир по-новому.

значок металлический с логотипом значки металл срочно москва

значок металлический цена металлические значки на заказ

значок металлический цена https://metallicheskie-znachki213.ru/

металлические значки москва изготовление металлических значков на заказ москва

значки круглые металлические изготовление металлических значков москва

металлический значок ссср заказ значков из металла со своим дизайном москва

лак после циклевки паркета паркет циклевка покрытие спб

Старый паркет? шлифовка дубового паркета профессиональное восстановление деревянного пола без пыли и лишних затрат. Удаляем царапины, потемнения и старое покрытие, возвращаем гладкость и естественный цвет. Используем современное оборудование, выполняем циклевку, шлифовку и лакировку паркета под ключ с гарантией качества и точным соблюдением сроков.

Read More: https://www.rootsclinicindia.com/totally-free-relationship-video-4k-hd-zero-watermark-down-load-now/

Today’s Focus: https://aibj.com.br/sem-categoria/solverde-casino-online-100-ate-500-bonus-solverde/

Recommended reading: https://lirat.org/explicit-bangla-sex-videos-of-a-great-pervert-along-with-his-next-door-neighbor-pornography-movies/

Skip to details: https://www.theprepperdome.com/indian-web-show-frre-ullu-pornography-movies/

Only the best is here: https://www.samanthawiraatmaja.com/godly-wives-dealing-with-your-husbands-pornography-addiction-by-sheila-gregoire/

Expanded article here: https://briketai.top/2026/03/16/descubra-os-melhores-acao-boas-vindas-2025/

Today’s highlights are here: http://www.the-glamorous-visual.com/?p=241315

PUPIL OF FATE MOTORS https://auto.ae/pupiloffatemotors автосалон премиум авто в Дубае. Продажа роскошных автомобилей, эксклюзивные модели и индивидуальный подбор. Помогаем выбрать, оформить и доставить авто с гарантией качества и высоким уровнем сервиса.

Эко-бытовая химия http://reporter63.ru/content/view/784903/himiya-dlya-uborki-sekrety-effektivnosti-i-bezopasnosti в Санкт-Петербурге — средства для уборки без вредных компонентов. Эффективная очистка, безопасность для здоровья и окружающей среды. Широкий ассортимент и доставка по городу.

Последние публикации: https://detivmodnom.ru/

Modern earth fault indicator monitor the condition of electrical networks and protect equipment. They offer rapid fault detection, high accuracy, and reliability for industrial applications.

Только лучшее здесь: циклевка старого паркета

Лучший выбор дня: стоимость шлифовки паркета

Текущие рекомендации: https://shlifovka-parketa.ru

Все подробности по ссылке: циклевка паркета недорого

Самые актуальный новости новостной портал — свежие события, аналитика и репортажи. Политика, экономика, технологии и общество. Будьте в курсе последних новостей и ключевых событий каждый день.

Kent Casino kentcasino.ru.com официальный сайт, регистрация и бонусы. Онлайн казино с быстрым выводом средств, слотами и играми от топ провайдеров. Получите фриспины и играйте на реальные деньги безопасно.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Volvo спецтехніка https://linktr.ee/spetstekhnika екскаватори, фронтальні навантажувачі та дорожні машини. Надійність, ефективність і сучасні рішення для будівництва. Продаж, підбір і обслуговування техніки для бізнесу.

Профессиональная: оклейка авто антигравийной пленкой – сохраните родное лакокрасочное покрытие в идеальном состоянии на долгие годы.

Полезный материал, рекомендую, что такое генерация ии

Нейросеть онлайн — лучшие сервисы https://vc.ru/aihub/2842517-luchshie-neuroseti-onlajn-dlya-rossii-obzor-2026-goda

Stackshine en.stackshine.io a SaaS cost management platform: subscription control, usage transparency, renewal tracking, and employee offboarding. Optimize your budget and reduce unnecessary software costs.

как оживить фото с девочкой https://vc.ru/aihub/2842518-ozhivlenie-foto-neurosetyu

Уничтожение вредителей https://dezinfekciya-mcd.ru/unichtozhenie/klopov/ уничтожение бактерий, вирусов и насекомых. Обработка квартир, домов и коммерческих помещений. Безопасные препараты, опытные специалисты и гарантия результата.

Free online games poki.com.az play without downloading or registering. A large collection of games across various genres: action, puzzles, racing, and strategy. Easily access from any device.

Arizona sports events https://oxu-az.com.az football, transfers, and live match results. Latest news, statistics, and reviews for fans and sports enthusiasts.

https://mine-drop1.com/

Free online games https://1001-oyun.com.az the best browser games with no installation required. Huge selection of genres, easy search, and quick launch. Play anytime for free.

Roblox Download delta-roblox Download the game, learn about Roblox Studio features, and learn about security settings. Play, create your own worlds, and protect your account. A complete guide to installing, playing, and using the platform safely.

Выгодно купить кварцевый песок для пескоструйного аппарата – 100% очистка без забитых сопел! Забудьте о засорах: очищайте металл в разы быстрее. Ваш аппарат скажет спасибо, а результат поразит клиента. Купить кварцевый песок!

майнкрафт казино играть онлайн

лучшие нейросети для создания приложений https://vc.ru/aihub/2842546-luchshie-besplatnye-neyroseti-2026-goda

казино майндроп

Нужен займ? срочный займ без лишних формальностей оформление онлайн без справок и поручителей. Быстрое решение, удобная подача заявки и получение денег на карту. Подберите выгодное предложение и получите средства в короткие сроки.

нейросеть для ответов: https://vc.ru/aihub/2842517-luchshie-neuroseti-onlajn-dlya-rossii-obzor-2026-goda

Только свежие новостной портал свежие новости политики, экономики, общества и технологий. Актуальные события, аналитика, обзоры и мнения экспертов. Следите за главными новостями страны и мира онлайн в удобном формате каждый день.

Строительные технологии https://universalstroi.su выгодные инвестиции в доступное жилье. Стабильный доход, перспективные проекты и высокий спрос. Получайте прибыль от инновационных решений в строительстве.

Шестигранные болты востребованы в проектах, где крепеж должен работать стабильно, а монтаж должен идти быстро и без лишних сложностей Это удобно для регулярных поставок и серийной сборки: саморезы оптом москва

Монтажные работы https://montazhstroy.su услуги по установке инженерных систем и конструкций. Быстро, качественно и с гарантией. Выполняем задачи любой сложности для частных и коммерческих объектов.

возврат ответственного хранения стоимость склада ответственного хранения

Благодаря грамотной планировке капсульный дом не создает ощущения ограниченного пространства, https://super-domiki.ru/

1win download

дизайн интерьера услуги разработка дизайн проекта интерьера квартиры

Complete insomnia treatment guide — understand causes, manage symptoms, and explore solutions. From lifestyle changes to therapies, learn how to achieve deep, restful sleep and improve daily performance.

заказать дизайн интерьера дизайнер квартир недорого

Хороший интернет магазин с понятным сайтом и нормальным отношением к клиенту. После оформления заказа долго ждать не пришлось, менеджер сразу всё подтвердил. Телефон доставили быстро, внешний вид и комплектация полностью соответствуют описанию. Остался доволен покупкой – сайт продажи телефонов

https://metallicheskiy-shtaketnik.ru/

Открываешь кейсы KC? easydrop промокод 15 актуальные бонусы и скидки для пользователей. Получайте выгодные предложения, дополнительные возможности и экономьте при использовании сервиса. Все действующие промокоды в одном месте.

Онлайн займы без отказа на https://credit-world.ru – это возможность получить деньги без лишних сложностей без лишних проверок и сложных условий. На сайте представлено более 50 МФО, где реально оформить займ даже при нестандартной ситуации. Сравните условия разных компаний, найти лучший вариант и подать заявку за несколько минут, получив решение практически сразу.

Office for rent https://rentofficetoday.com/en/ business premises in business centers and commercial buildings. Compare office for rent, private office space for rent, and offices to rent in prime locations. Find the best office rental solutions and rent office space that fits your business needs

противопожарные двери https://dveri-ot-zavoda.ru с доставкой и профессиональной консультацией, посмотрите актуальные решения для разных типов помещений.

Сломалась машина? выездная помощь на дороге по машинам техпомощь на дорогах СПб и Ленобласти: эвакуация, подвоз топлива, запуск двигателя, вытаскивание авто — 24/7. Круглосуточная мобильная служба техпомощи в Санкт?Петербурге и Ленинградской области. Оказываем выездную помощь в любое время: эвакуируем авто, подвозим топливо, помогаем завести двигатель и вытаскиваем застрявшие машины.

Универсальный флагманский безбумажный регистратор jumo logoscreen 700 для контроля температуры, давления и других технологических параметров. Удобный интерфейс, точные измерения и возможность интеграции в системы мониторинга.

Нужен промокод? easydrop промокоды актуальные бонусы, скидки и акции для пользователей. Используйте рабочие коды, получайте дополнительные преимущества и экономьте при использовании сервиса. Все свежие предложения в одном месте.

Нужна брендированная продукция? https://2ymedia.kz/category/sumki/ ваш надежный партнер в сфере брендинга в Алматы. Мы специализируемся на производстве сувенирной продукции с нанесением логотипа и корпоративной полиграфии. В нашем каталоге вы найдете всё для продвижения бренда: бизнес-сувениры, промо-мерч, текстиль и полиграфическую продукцию. Мы принимаем заказы оптом от 50 единиц, что делает нас доступными как для крупного бизнеса, так и для небольших компаний.

Гранитные памятники https://allgranit.ru от производителя в Москве: надёжность и красота на века. Компания Allgranit предлагает гранитные памятники напрямую от производителя — без посредников, переплат и долгих ожиданий. Мы создаём мемориалы, которые сохраняют память о дорогих людях на долгие годы.

Нужен ремонт? ремонт квартиры по смете под ключ, быстро и качественно. Дизайн, отделка, электрика и сантехника. Гарантия на работы и прозрачная смета. Выполняем проекты любой сложности.

Проблемы с алкоголем? https://www.narkolog-na-dom-vizov.ru срочная помощь при алкогольной и наркотической интоксикации. Вывод из запоя, капельницы и поддержка 24/7. Анонимно, быстро и безопасно с выездом врача на дом.

https://starcasino-au.com/

Лучшее путешествие джип тур авто горы, каньоны и побережье. Увлекательные маршруты, опытные гиды и яркие впечатления от путешествий по Крыму.

Do you trade cryptocurrencies? bitkelttrade platform automate your transactions and earn passive income. Smart algorithms analyze the market and help you make decisions. Increase your income and reduce risks with modern technology.

Надёжный партнёр компрессорное масло купить для оптовых закупок масел и антифризов в бочках по всей России.

החלה למצוץ בביישנות, תחילה ליקקה את ראשה בלשון. אבל אחרי כמה או שלוש דקות, היא, כמו שאומרים, התפוגגה, והתחילה למצוץ באופן פעיל יותר, בהנאה נראית לעין, להכות ולטבול את הזין בפה שלה אחר! “אבל אתה אוהב את סרגיי,” הוא אמר פתאום, מתבונן מקרוב בתגובתה. סרגיי. עמית. אותו אחד שהבדיחות שלו תמיד הצחיקו אותה ונגיעות מקריות גרמו לה להסמיק. זה לא אני לא מקסים גיחך — הוא https://best-ayianapa.co.il/

Marka Vavada pojawiła się na scenie w 2017 roku z garścią slotów w ofercie. Od tamtej chwili przeszła długą drogę – dziś w jej katalogu znajdziesz nie tylko automaty, lecz także klasyczne gry stołowe, jackpoty i rozbudowane kasyno na żywo. Z lokalnego debiutanta Vavada stała się graczem globalnym, a w Polsce zdobyła sympatię użytkowników dzięki prostym zasadom, licencji Curaçao oraz wygodnym płatnościom w złotówkach. To konsekwentne podejście sprawia, że marka systematycznie wzmacnia swoją pozycję w świecie iGamingu.

Лучшее путешествие джип туры ялта горы, каньоны и побережье. Увлекательные маршруты, опытные гиды и яркие впечатления от путешествий по Крыму.

Do you trade cryptocurrencies? learn more about bitkelttrade automate your transactions and earn passive income. Smart algorithms analyze the market and help you make decisions. Increase your income and reduce risks with modern technology.

https://mhp.ooo/products/slimshape-120

Подробности на странице: https://home-parfum.ru/catalog/memo/

ГНБ бурение https://stroytex.su современный способ прокладки инженерных сетей без раскопок. Подходит для дорог, рек и плотной застройки. Точная технология, сокращение сроков и минимальные затраты.

флаг с надписью на заказ флаг на заказ спб

Хочешь оригинальную подушку? заказать подушку дакимакуру комфорт и уют для сна. Длинная форма, мягкий наполнитель и стильные принты. Отлично подходит для отдыха и расслабления.

Нужен пластический хирург? клиника центр пластической хирургии современные операции и эстетические процедуры. Опытные хирурги, безопасные методики и индивидуальный подход. Консультации, диагностика и качественный результат.

Нужна мебель? изготовление мебели на заказ эксклюзивные изделия из натурального дерева. Индивидуальный дизайн, качественные материалы и точное изготовление. Решения для дома и бизнеса.

казино онлайн дают азартной игры с минимальными ставками, официальный сайт плей фортуна

Нужна премиум мебель? https://premialnaya-mebel.ru изготовление на заказ. Натуральные материалы, эксклюзивный дизайн и долговечность. Решения для дома и бизнеса с высоким уровнем качества.

мебель на заказ премиум сайт премиум мебели

Доставка свежих цветов в день заказа. Флористы собирают букеты из проверенных поставок, бережно упаковывают и передают курьеру. Работаем ежедневно, гарантируем сохранность и точное время вручения. Анонимная отправка и фотоотчёт включены https://buketico.ru/

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Полная статья здесь: https://sn74.ru

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

https://dogs-tula.ru/

Your article helped me a lot, is there any more related content? Thanks!

Комплексный анализ в https://npprteam.shop/articles/reddit/luchshee-vremja-postov-reddit-2026-gajd-sabreddity/ объединяет исследовательские данные, статистику активности и практические примеры успешных кампаний на Reddit. Материал освещает региональные особенности временных зон, влияние сезонности на активность аудитории и эффект информационных повесток на количество взаимодействий. В гайде приведены конкретные временные окна для различных целевых аудиторий — от студентов и фрилансеров до корпоративных профессионалов и предпринимателей. Эта информация критически важна для тех, кто планирует масштабировать свою присутствие на Reddit как в целях органического трафика, так и в контексте интеграции с платными кампаниями. Использование рекомендаций из гайда позволит значительно повысить CTR, увеличить количество апвотов и комментариев, а также установить стабильный график публикаций, соответствующий особенностям каждого сабреддита.

No te quedes con las ganas — abre rajajoy-mx.com y empieza a disfrutar.

При выборе сравнение цен на цифровые товары между официальными магазинами и реселлерами становится первым побуждением любого экономного покупателя, но цена — не единственный фактор в уравнении. Маркетплейсы действительно предлагают более низкие цены, однако они сопряжены с серьезными рисками: покупка украденных ключей, блокировка аккаунта, отсутствие гарантии возврата и потенциальная потеря доступа к уже купленной игре. Официальные платформы, хотя и дороже, гарантируют легальность ключа, соответствие региональным требованиям и возможность решить проблемы через техническую поддержку. Разница в гарантиях между официальными магазинами и реселлерами может составлять не просто несколько сотен рублей, но и потерю всего вашего игрового инвентаря. Для серьезных игроков, инвестирующих в цифровую библиотеку, эта гарантия стоит того, чтобы переплатить несколько процентов при покупке через лицензированные каналы.

Хранение влияет на порядок на кухне https://medyn.su/kuhonnaya-tekhnika/organizaciya-khraneniya-vydvizhnye-sistemy-i-kargo/

Se vuoi valutare una piattaforma orientata al mercato italiano https://alfcasinowin.it con un’impostazione pratica per esplorare giochi e aree importanti puo rappresentare un’opzione valida da esaminare mentre analizzi opzioni adatte al mercato italiano per mostrare giochi conosciuti, categorie ben separate, esperienza confortevole, impostazione pratica, accesso rapido e attenzione all’utente.

коли свято святої Алли

If you want to browse a notes-style resource in the gambling niche https://plicpad.com with organized content and quick access to the main sections can give you a useful overview if you want to compare different gambling-related resources by combining clarity, variety, ease of use, effective organization, well-distributed content, intuitive access and practical reading comfort.

buy cannabis

gay anime porn

incest porn stories

Искал магазин, где можно спокойно купить телефон без риска и неприятных сюрпризов. Здесь всё прошло очень ровно: быстро приняли заказ, вежливо проконсультировали и вовремя отправили покупку. Смартфон оказался именно таким, как в описании. Надёжный вариант для тех, кто ценит нормальный сервис – интернет магазин по продаже телефонов

детские студии спб

A couple of days ago I stopped by to evaluate a casino site.

To begin with I was curious to see the interface and game catalog, mostly for comparison. In the end the platform gave a fairly decent impression: the site structure looked logical,

at the same time I noticed a fairly diverse catalog. Another thing seemed convenient, that the information and games are arranged quite conveniently, and this makes the experience more comfortable.

In addition it’s worth mentioning convenient deposit and withdrawal methods,

which also makes the service more convenient. Naturally

I can’t say that the site has no weak points, still it’s

clear that work was clearly done on usability here.

As for me it’s better to remember your personal limits,

as comfort depends on a reasonable approach. If someone wants to form their own opinion, in that case you can explore the platform yourself.

If you take into account convenience and overall presentation, then personally

for me no serious questions came up. Link:

Vegazone play

Are you looking for a fast, safe and hassle-free transfer in Valencia? We offer professional transport and moving services, both for individuals and companies. Request your budget without obligation and enjoy a quality service https://trasladoavalencia.es/

как перестать обновлять мужа к бывшей жене практические советы техники уверенности и шагов к спокоиствию

для чего нужно помнить в видеокарте за что отвечает объем и на что влияет видеопамять

Нужны ли отдельные страницы под каждый город при Гео оптимизации сайта? Гео оптимизация сайта

Продвижение сайтов в google в нише с низким поисковым спросом — есть ли смысл?

Как быстро происходит Разработка сайтов для интернет-магазина с большим каталогом?

Чому високі тригліцериди

Какие домашние животные можно держать без специального разрешения?

Online gaming directories are useful for visitors to compare offers before choosing where to play. dragonia7casino.de can be used as a localized gaming page. A good page should stay clear and informative and make navigation straightforward.

Поисковое продвижение сайта — как выстроить грамотную контент-стратегию?

Как отследить эффект от Гео оптимизации сайта в аналитике? [url=https://geo-optimizaciya-sajta.ru]Гео оптимизация сайта[/url]

Капсульный дом — что важно проверить при приёмке готового объекта?

Serm — как правильно работать с негативными отзывами на специализированных площадках?

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

sailing Montenegro https://rent-a-yacht-montenegro.com

yacht charter Montenegro rent a yacht Montenegro

Нужен сайт? разработка сайта под ключ в компании domenanet.by. Профессиональная разработка сайтов любой сложности в Минске: от интернет-магазинов до порталов.

Если нужен недорогой аккумулятор https://www.akb24v.ru 24 вольта для погрузчика, стоит обратить внимание на проверенные решения с оптимальным ресурсом и стабильной отдачей. Купить тяговую батарею 24V можно на сайте, там представлены варианты под разные задачи и типы техники.

Понравилось, что всё прошло без лишней суеты и строго по договорённости. Девушка вежливая и внимательная. Атмосфера спокойная и располагающая. Сервис продуман – высокие проститутки

читать последние новости россии новости хоккея и фигурного катания

Читать расширенную версию: https://spainslov.ru/site/word/word/%D0%91%D0%90%D0%A8%D0%90

Live football scores https://canli-futbol.com.az up-to-date schedules, and league tables. Follow matches, check scores online, analyze team standings, and never miss a beat in world football.

All football match https://canli-skor.com.az results online, game schedules, and league standings. Live updates, statistics, and easy access to information about matches and teams from around the world.

Baky ucun deqiq hava proqnozu. Bu gun, sabah ve hefte ucun temperaturu, yagini? ehtimalini, kuleyin sгrуtini му hava seraitini onlayn yoxlayin.

Phasmophobia Game 2026 https://phasmo-phobia.com is a cross-platform horror game supporting PC, PlayStation, Xbox, and VR. Find out the game’s current price, platform list, system requirements, and the latest updates with new maps, events, and gameplay improvements.

На порталі https://visti.pl.ua зібрані головні новини Полтави та області. Тут публікують матеріали про події, транспорт, інфраструктуру та життя регіону.

Сайт https://news.vinnica.ua висвітлює події у Вінниці та регіоні. Новини, аналітика й корисні матеріали допомагають бути в курсі життя міста щодня.

На порталі https://krivoy-rog.in.ua зібрані головні новини Кривого Рогу. Тут публікують матеріали про події, транспорт, інфраструктуру та життя мешканців.

На сайті https://gazeta-bukovyna.cv.ua публікують свіжі новини Буковини та Чернівців. Тут ви знайдете актуальну інформацію про події, життя регіону, культуру й важливі зміни для мешканців.

На сайте https://chernomorskoe.info собраны новости Черноморского побережья и информация о курортных городах Одесской области. Узнавайте о событиях, отдыхе и развитии региона.

На портале https://o-remonte.com вы найдёте статьи о ремонте, дизайне и строительстве. Сайт предлагает практичные решения, рекомендации и идеи для создания уютного пространства.

It’s awesome to pay a quick visit this web page and reading the views of all mates concerning this post, while I am also zealous of getting experience.

kasiino kampaaniad

Продажа медицинской техники https://techmed.kz и оборудования в Алматы от компании Adamant Group — это сертифицированные УЗИ-сканеры, физиотерапевтические, лабораторные и хирургические аппараты от надёжных производителей. Работаем с 2004 года, предлагаем сервис, установку и гарантию на всё оборудование. Медицинские аппараты с доставкой по Казахстану — оперативно отгружаем в любую точку страны, помогаем с подбором под задачи вашей клиники.

Нужен керамзит? https://l-keramzit.ru/keramzit-v-meshkah/ качественный керамзит различных фракций для утепления, дренажа и производства легкого бетона. Доступны оптовые поставки, удобная упаковка и доставка на объект.

смотреть воронины стражи гробниц 2018 смотреть онлайн

безславні виродки дивитись онлайн джек ричер

нічого качині історії

еліо в густом лесу

эвакуатор круглосуточный эвакуатор авито по москве

Продажа песка https://pesok-krd.ru и щебня в Краснодар с доставкой по городу и области. Качественные нерудные материалы для строительства, благоустройства и дорожных работ. Доступны разные фракции, оптовые и розничные поставки.

Plan your journey with https://ko.readytotrip.com, online hotel booking for any destination worldwide. Instant reservation, transparent prices, and no hidden fees. Trusted platform for hassle-free travel arrangements. Start booking today.

Нужен выездной ресторан? кейтеринговая компания с доставкой и обслуживанием на вашей площадке. Фуршеты, банкеты, кофе-брейки и барбекю для деловых и праздничных мероприятий. Профессиональная организация питания и широкий выбор блюд для гостей.

Женский портал https://secretlady.ru с полезными статьями о красоте, здоровье, моде, отношениях и саморазвитии. На сайте собраны советы экспертов, идеи для вдохновения, рецепты, лайфхаки и актуальные темы для современной женщины.

Недорогие аккумуляторы https://www.akb24v.ru 24 вольта для погрузчика, стоит обратить внимание на проверенные решения с оптимальным ресурсом и стабильной отдачей. Купить тяговую батарею 24V по доступной цене. Варианты под разные задачи и типы техники.

Interested in UFC? https://ufc-white-house.com unique mixed martial arts tournament will take place on June 14, 2026, in Washington, D.C., on the South Lawn of the White House. It will be the first professional sporting event in history to be held directly on the grounds of the U.S. presidential residence.

ремонт стиралки фирмы по ремонту стиральных машин

казино вулкан казино х

8stars https://888starz-uz1.org/ .

888starz. https://888starz-egypt9.com/

remove stains from sofa

Частный гид по Калининграду проведёт Калининград обзорная экскурсия по городу индивидуальные с экскурсоводом и персональным маршрутом по достопримечательностям города.

8888 bet 888starz-uz3.org .

наруто смотреть онлайн наруто смотреть онлайн бесплатно в хорошем

адрес стоматологии номер стоматологии

лечение в наркологическом стационаре лечение в наркологическом стационаре

вызов нарколога на дом в москве вызов нарколога на дом в москве

врач нарколог на дом врач нарколог на дом

наркологический стационар в спб наркологический стационар в спб

вызов врача нарколога на дом срочный выезд вызов врача нарколога на дом срочный выезд

вызов нарколога на дом круглосуточно москва вызов нарколога на дом круглосуточно москва

нарколог на дом анонимно москва нарколог на дом анонимно москва

gundem xeberleri euro mezennesi

наркологический стационар в спб наркологический стационар в спб

выезд нарколога на дом цена выезд нарколога на дом цена

эвакуатор межгород эвакуатор с погрузкой

выезд нарколога на дом цена выезд нарколога на дом цена

neviditelne sluchatko mikrosluchatko

наркологический стационар санкт петербург наркологический стационар санкт петербург

услуги нарколога на дому услуги нарколога на дому

продвижение сайта в интернете kormclub.ru

«Кракен-зеркала» — это альтернативные адреса сайтов, которые появляются после блокировок или технических сбоев. Пользователи часто ищут такие ссылки для доступа к ресурсу, однако важно помнить о рисках: мошеннические копии могут похищать данные, пароли и криптовалюту. Эксперты по кибербезопасности рекомендуют проверять адреса сайтов и не переходить по сомнительным ссылкам.кракен даркнет v5tor cfd

888 stars https://uz888-starz.com .

Хочешь ремонт? ремонт квартир в Омске — профессиональные услуги по ремонту квартир любой сложности: косметический, капитальный и дизайнерский ремонт с гарантией качества и индивидуальным подходом.

The real estate market on the Costa Blanca continues to grow, making сonstruction Moraira an attractive option for clients seeking long-term investment, modern architecture and high-quality bespoke villas with strong resale value.

анальное порно casino selector

8starz https://888starz-egypt5.com/

Автомобильный портал https://autort.ru с обзорами машин, новостями автопрома, рейтингами моделей и советами по выбору авто. Полезная информация для покупателей, владельцев и всех любителей автомобилей.

Женский портал https://justwoman.club с полезными статьями о красоте, здоровье, моде, психологии и отношениях. Советы экспертов, лайфхаки, идеи для ухода за собой и вдохновение для современной женщины.

дренаж лица в косметологии что

Таможенное оформление для юридических лиц в Москве и Московской области. СБ Карго – официальный таможенный представитель: подготовка документов, расчёт платежей, сопровождение импорта и экспорта, помощь в прохождении таможенных процедур без лишних рисков и задержек. Консультации для участников ВЭД: Таможенное оформление грузов в аэропорту

Сейчас удобно выбирать дорамы 2026 онлайн без десятков открытых вкладок, непонятных ресурсов и бесконечных вкладок. DoramaLend объединил в одном месте корейские, китайские, японские и другие азиатские сериалы с понятным русским переводом, удобными описаниями, разделами по жанрам, годами выхода и простыми карточками сериалов. Здесь легко найти романтическую историю на вечер, динамичный триллер, сериал для хорошего настроения или свежую новинку, которую уже обсуждают поклонники дорам.

1win demo kazino 1win demo kazino

Текущие рекомендации: https://spainslov.ru/site/word/word/%D0%9E%D0%91%D0%AA%D0%AF%D0%A2%D0%98%D0%95

«Кракен-зеркала» — это альтернативные адреса сайтов, которые появляются после блокировок или технических сбоев. Пользователи часто ищут такие ссылки для доступа к ресурсу, однако важно помнить о рисках: мошеннические копии могут похищать данные, пароли и криптовалюту. Эксперты по кибербезопасности рекомендуют проверять адреса сайтов и не переходить по сомнительным ссылкам.рабочая ссылка на кракен

1win qo‘llab-quvvatlash Oʻzbekiston 1win39427.help

Легендарная охота за богатствами продолжается! Новые загадки древних династий, опасные экспедиции и тайны, скрытые веками. Кто разгадает шифры прошлого и доберётся до бесценных артефактов? Захватывающие повороты, рискованные ставки и неожиданные союзники ждут тебя: https://sokrovischa-imperatora-3-sezon.top/

1win registratsiya 2026 https://www.1win39427.help

mostbet cod sms mostbet cod sms

Для тех, кто хочет дорамы с русской озвучкой спокойно, без лишних переходов и путаницы, DoramaGo может стать хорошим вариантом для отдыха после учебы или работы. Здесь представлены корейские, китайские, японские, тайские и другие азиатские сериалы, где есть то самое настроение, за которое дорамы так ценят: нежные и драматичные истории, интриги, яркие герои и визуальная красота азиатских сериалов. Удобный каталог помогает выбрать историю под настроение по стране, жанру, году или настроению, а свежие серии позволяют следить за любимыми проектами.

Смотрите русские сериалы https://top-tvshou.ru и ТВ-шоу онлайн бесплатно в хорошем качестве. Большая коллекция популярных проектов, новые серии и любимые телепередачи. Удобный каталог, быстрый поиск по жанрам и актерам, возможность смотреть на компьютере, планшете и смартфоне без регистрации.

موقع 8888 stars 88

Арена гайдов crarena.ru полезные гайды по играм, квестам и заданиям. Подробные прохождения, советы, секреты и тактики для разных игр. Помогаем быстрее проходить миссии, находить скрытые предметы и открывать новые возможности игрового мира.

888starz сайт 888starz сайт .

888starbet 888starbet .

888syarz 888syarz .

télécharger melbet sur téléphone télécharger melbet sur téléphone

تسجيل الدخول 888starz https://888starz-egyp.com/

888starz تسجيل الدخول https://888starzeg1.com/

mostbet visa mostbet visa

888starz login 888starz login .

888srarz https://888starz-eg2.org/

888starz تسجيل الدخول مراهنات كازينو 888 تسجيل الدخول

Новостной онлайн-портал https://vse-novosti.net с круглосуточным обновлением информации. Новости мира и регионов, аналитические материалы, обзоры и важные события в одном месте.

Новостной портал https://tovarpost.ru с актуальными событиями России и мира. Политика, экономика, общество, технологии и спорт. Оперативные новости, аналитика и важные события в режиме реального времени.

1win app free download https://1win3003.mobi/

mostbet intrare pe site oficial mostbet intrare pe site oficial

1win free spins qayerda 1win free spins qayerda

Хочешь узнать про электронные чеки? электронные чеки для ип важный этап цифровизации торговли и налогового контроля. Узнайте, как работают электронные чеки, какие преимущества они дают бизнесу и покупателям, а также какие изменения ждут предпринимателей.

aviator trusted site malawi aviator trusted site malawi

Материал о том, как утеплить водопроводные трубы в доме, на даче или в неотапливаемых зонах. Рассматриваются виды теплоизоляции, защита от промерзания, прокладка греющего кабеля, типичные ошибки монтажа и ситуации, когда простого утеплителя уже недостаточно https://santexnik-market.ru/inzhenernaya-santehnika/uteplenie-vodoprovodnykh-trub/

«Кракен-зеркала» — это альтернативные адреса сайтов, которые появляются после блокировок или технических сбоев. Пользователи часто ищут такие ссылки для доступа к ресурсу, однако важно помнить о рисках: мошеннические копии могут похищать данные, пароли и криптовалюту. Эксперты по кибербезопасности рекомендуют проверять адреса сайтов и не переходить по сомнительным ссылкам.kraken сайт официальный 2kmp pro

1win bonus conditions https://1win3003.mobi/

1win app not working 1win app not working

melbet aviator avis https://melbet62913.help

mostbet depunere Republica Moldova http://mostbet18305.help/

how to get 1win free spins http://1win3003.mobi/

melbet pari tennis https://melbet62913.help/

aviator visa withdrawal http://aviator50638.help/

aviator plinko signals https://aviator50638.help

mostbet limită retragere https://www.mostbet41079.help

mostbet əməliyyat gözləmədə mostbet əməliyyat gözləmədə

1win aviator cum se joaca 1win5757.help

Красоты мурманска тур в териберку из спб заполярная романтика, суровое Баренцево море и северное сияние, которое здесь ловят с сентября по апрель. Мы организуем тур в Мурманск из Москвы и туры в Мурманск из СПб с комфортом и без лишних пересадок. Принимаем туристов в Мурманске из любого региона России.

comment jouer à mines sur melbet http://www.melbet62913.help

888starz.bet https://www.888stars-uz.com .

When finance teams struggle with spreadsheets and email chains, implementing a structured capex approval workflow ensures every major purchase is properly reviewed, compliant, and tracked from request to final sign-off.

Initial testing: buy 50 tiktok likes first to verify provider reliability before committing to larger investments.

mostbet parola uitata mostbet parola uitata

mostbet rezultate live mostbet rezultate live

aviator malawi website aviator50638.help

1win mirror curent 1win5757.help

«Кракен-зеркала» — это альтернативные адреса сайтов, которые появляются после блокировок или технических сбоев. Пользователи часто ищут такие ссылки для доступа к ресурсу, однако важно помнить о рисках: мошеннические копии могут похищать данные, пароли и криптовалюту. Эксперты по кибербезопасности рекомендуют проверять адреса сайтов и не переходить по сомнительным ссылкам.кракен гидра

Новостной портал https://press-center.news с актуальными событиями из мира политики, экономики, технологий, общества и культуры. Оперативные новости, аналитические материалы, интервью, репортажи и мнения экспертов. Следите за важными событиями в стране и мире в удобном формате.

mostbet ekspress əmsal http://mostbet01859.help/

mostbet vklad mostbet vklad

mostbet přístup http://www.mostbet87124.help

1win download Republica Moldova 1win download Republica Moldova

Останні новини https://18000.ck.ua Черкас та Черкаської області

plinko pe mostbet http://mostbet18305.help

mostbet rulet http://mostbet01859.help/

mostbet şifrə tələbləri mostbet01859.help

mostbet sázky čeština https://www.mostbet87124.help

mostbet sázky na hokej https://www.mostbet87124.help

Нужна CRM банкротством физ лиц? битрикс24 для БФЛ инструмент автоматизации юридического бизнеса по банкротству физических лиц. Управляйте заявками, делами клиентов, документами и сроками процедур. Система помогает организовать работу команды и контролировать каждый этап банкротства.

1win Soroca 1win Soroca

ШіШЄШ§Ш± 888 Щ„Щ„Щ…Ш±Ш§Щ‡Щ†Ш§ШЄ https://888starzeg2.com/

88starz apk وان اكس بت 888

888starz apk download تنزيل ٨٨٨ ستارز

888bet skachat 888bet skachat .

888starz apk https://world-cuisine.com/

Промокоды магазина Пятёрочка https://www.time-samara.ru/content/view/785106/transformaciya-sistemy-loyalnosti-v-sovremennom-rossijskom-ritejle актуальные скидки, акции и специальные предложения для выгодных покупок. Найдите рабочие промокоды, купоны и бонусы, чтобы экономить на продуктах, товарах для дома и повседневных покупках.